Let’s Get to the Bottom of These Credit Myths

Checklist to Prepare Your Personal Finances in the New Year

01/20/2023

Want to Protect Your Credit? Try a Savings Challenge

01/28/2023

Myths and misinformation about credit scores, credit reports, and credit repair are extremely common. Unfortunately, many people believe these myths, and their credit suffers as a result of taking incorrect actions.

Let’s get to the bottom of these credit myths and learn the truth about them so you can start improving your credit the right way.

Myth: Everyone automatically has a credit score.

Fact: 1 in 5 adults in the United States do not have credit scores.

A report by the Consumer Financial Protection Bureau (CFPB) found that one-fifth of adults in the United States do not have enough credit data to calculate a credit score by traditional methods. These consumers are called “credit invisibles.”

Low-income consumers are particularly susceptible to credit invisibility due to a lack of access to traditional credit products. Some consumers may be credit invisible for other reasons, such as a voluntary decision not to use credit.

For those that do not use credit for whatever reason, it is likely that they do not have enough credit history to generate a credit score.

Consumers that are credit invisible may be able to generate a credit record by piggybacking on the good credit of others, but don’t assume that everyone has a credit score just by virtue of existing.

Myth: Checking your credit report will hurt your credit score.

Fact: Checking your own credit will not hurt your score.

About one in five Americans are credit invisible, which means they do not have credit scores.

Checking your own credit report results in what is known as a “soft pull,” which means the inquiry does not affect your credit score.

To understand the difference between hard and soft inquiries and how they affect your credit score, see our article, “Are Inquiries Really Killing Your Credit?”

Myth: Your income affects your credit score.

Fact: Your credit score does not look at your income.

However, your income can affect your credit indirectly in that it influences the “five C’s” that have been shown to predict credit performance: capacity to pay off debts, the collateral backing a loan, capital available to repay a loan, conditions that affect income and expenses, and the character of the borrower.

Your capacity to pay off debts as well as the collateral and capital they have available to repay loans may all have a relationship with your income.

That’s a big part of the reason why low-income consumers are 8 times more likely than high-income consumers to have no credit score at all. In consumers that do have credit scores, those who reside in low-income areas have lower credit scores. In addition, low-income consumers are 240 percent more likely to have their credit file originated due to derogatory items such as collections.

Each consumer can have dozens of different credit scores.

So while your income is not technically incorporated into your credit score, it can definitely influence your ability to repay debts, which is the basis of a credit score.

Myth: You only have one credit score.

Fact: There are many different credit scores.

There are two general types of credit scores: FICO scores, developed by Fair Isaac Corporation, and VantageScore, developed by the three major credit bureaus (Equifax, Experian, and TransUnion).

FICO 8 is the credit score most commonly by lenders today, but in some industries, older models or industry-specific models are used instead. For example, there are FICO scores tailored specifically toward auto loans and credit cards, and mortgage lenders are known to use the older FICO score versions 2, 4, and 5. Plus, FICO scores are different for each credit bureau.

VantageScore, which is increasingly used by some lenders as well as for consumer credit education, also has a few versions. The latest version is VantageScore 4.0, but VantageScore 3.0 is still the most commonly used version today.

Altogether, between the many versions of FICO scores and VantageScores, consumers can have dozens of different credit scores.

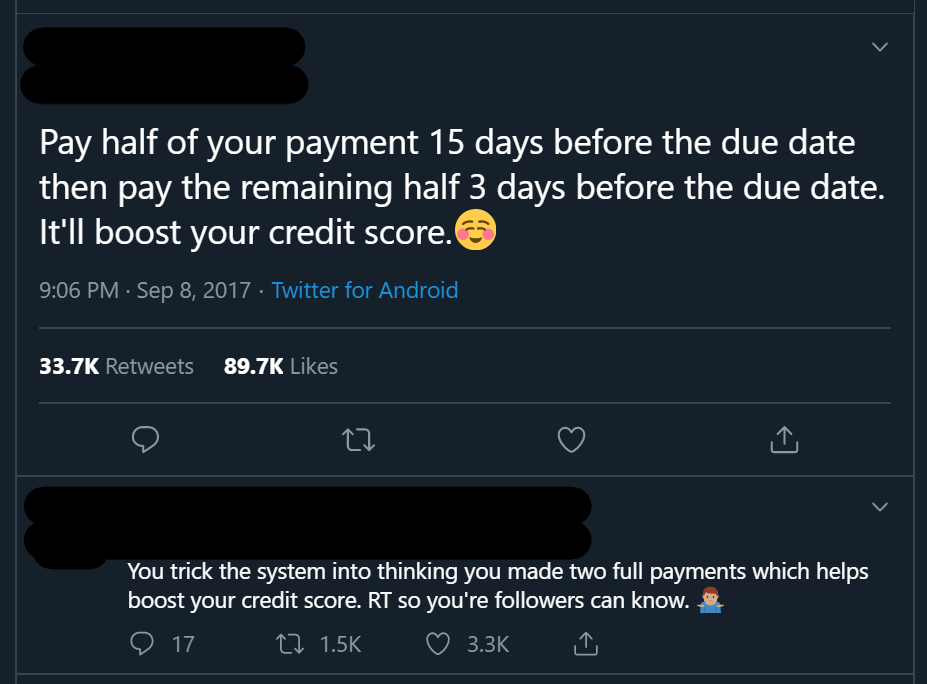

Myth: Paying half of your minimum payment twice a month counts as two full payments and tricks the system into giving you twice the credit score boost.

Fact: Dividing your bill in half and making two payments is the same as paying the full amount once.

This credit myth is unfounded yet often repeated.

If this “credit hack” sounds a little too good to be true, that’s because it is. It is simply not true that you can “trick the system” into thinking you have made two full payments by making two half payments.

Making a payment on a credit account affects two main factors of your credit score: payment history and credit utilization. Let’s discuss each factor individually.

When it comes to your payment history, making a partial payment that is less than the minimum amount due does not satisfy the requirement and will not count as an on-time payment. Only once you have made the second payment for the other half of the amount due will you have satisfied the requirement to be considered paid on time.

Therefore, you do not gain any extra benefit to your payment history from dividing your payment into two parts instead of paying the full amount at one time.

As an example, let’s say you have a bill due on the 30th and the minimum amount you must pay is $50. We have laid out the two payment scenarios in the table below.

| Scenario 1: Pay the full amount in one payment | Scenario 2: Make half of the payment twice | ||||

| Date | Amount Paid | Payment Status | Date | Amount Paid | Payment Status |

| 15th | 15th | $25 | Insufficient payment—$25 still due | ||

| 30th | $50 | Paid on time | 30th | $25 | Paid on time |

As you can see from the table, in both scenarios, you only get the benefit of paying your bill on time once per billing cycle, not twice.

Now let’s discuss the utilization factor. Continuing with the same example, the total amount you are paying toward the account is $50 in both scenarios. Therefore, the overall improvement in your utilization ratio is going to be the same either way.

If you don’t have any credit history, you can begin building credit by piggybacking on someone else’s good credit.

Now, if the reporting date for that account is between the first and second payments, since you have already sent a partial payment, you may temporarily get a small boost from having a slightly lower utilization ratio when the account reports to the credit bureaus. But at the end of the billing cycle, the result will be the same.

If you decide to make extra payments in addition to your minimum payment, which is ideally what all responsible borrowers should be doing, that can certainly help your credit score by speeding up your debt repayment. But simply splitting the minimum payment into two payments won’t do anything to boost your score.

Although this so-called credit hack unfortunately won’t help your credit very much, you can find some strategies that do work in our list of Easy Credit Hacks That Will Actually Get You Results.

Myth: If you don’t have a credit history, you’ll never be able to get credit.

Fact: You can start building credit by piggybacking.

While it can definitely be more difficult to get credit when you don’t have any credit history to begin with, it’s not impossible. There are credit products out there designed for people with no credit or bad credit, such as secured credit cards and credit-builder loans.

Another way to start building credit fast is by piggybacking off of the good credit of someone else. You could have someone you trust cosign on a loan or open a joint account with you, or you could become an authorized user on someone else’s seasoned tradeline.

If you are not lucky enough to know someone who has a seasoned account with perfect payment history that they could add you to, consider purchasing tradelines from a reputable tradeline company.

Myth: Paying off a collection will “re-age” the debt because the account falls off your credit report based on the date of last activity.

It is illegal to “restart the clock” on collections.

Fact: Collections fall off your credit seven years after the initial delinquency and cannot legally be re-aged.

If you’ve read our article about collections on your credit report, then you know that it is the date of first delinquency (DOFD) that determines when the collection will be removed from your credit report, not the “date of last activity” (DLA).

The reason why some people may believe this myth is because shady debt collectors sometimes illegally change the date of first delinquency to the date of last activity in an attempt to re-age the debt.

As we said, this practice is illegal. If you notice that a debt collector has improperly changed any information about a collection account on your credit report, you have the right to dispute the inaccurate information.

Myth: Paying off a collection will boost your credit score.

Fact: Paying off a collection may or may not raise your score depending on which credit score is used.

While it makes sense to assume that paying off a collection should increase your credit score, that is not always the case. In fact, more often than not, this is not the case, although it depends on which credit score is being used.

With FICO 8 and all previous FICO scores, both paid and unpaid collections are categorized as major derogatory items on your credit report. Therefore, paying off the account will not change how it is considered by the credit scoring algorithm, which means your score may not go up at all.

On the other hand, FICO 9, VantageScore 3.0, and VantageScore 4.0 ignore paid collection accounts, so your score should recover after paying off a collection if one of these credit scoring models is being used.

Myth: You should close accounts you’re not using.

Fact: You should keep accounts open and use them periodically.

Rather than closing credit cards you don’t use anymore, use them every so often to keep them open and in good standing.

While you might think that closing accounts you don’t need will help your credit score, the opposite is actually true, especially when it comes to revolving accounts such as credit cards.

The main reason for this is that credit utilization is an important part of your credit score, and closing credit card accounts will hurt your utilization ratio by decreasing your credit limit.

It could also hurt your mix of credit, although that’s a less important factor.

In addition, payment history is the number one factor that helps your score. It’s better for your credit to keep the account open, use it for small purchases here and there or a monthly subscription, and pay it off every month to keep building additional positive payment history.

The exception to this rule is if an account comes with an annual fee that’s no longer worth the price or if you can’t resist the temptation to overspend. In these cases, it might be better for your wallet to go ahead and close the account anyway.

Myth: Closed accounts don’t affect your credit.

Fact: Closed accounts can have a significant impact on your credit.

Although we just discussed why you shouldn’t necessarily close old accounts, that’s not to say that closed accounts don’t impact your credit. They certainly can, particularly when it comes to your credit age.

Closing an account does not remove its payment history or age from your credit report, so closed accounts still contribute to your credit age. In addition, accounts can continue to age even after they have been closed.

Carrying a balance on your credit cards is expensive and is not necessary to build credit. Photo by Hloom on Flickr.

So although it’s best to keep accounts open if you can, having closed accounts on your credit report is not a bad thing. If the account was closed in good standing, it will likely continue to help your credit.

Myth: Carrying a balance on your credit cards will help your credit.

Fact: Carrying a balance will not help you build credit and it will cost you interest fees.

While it is important to use credit regularly when building credit, it’s not necessary to carry a balance on your credit cards from month to month. If you do this in an attempt to build credit, you will be wasting money by paying unnecessary interest.

The best way to build credit using your credit cards is to use them responsibly and then pay the full balance due each month or even make multiple payments each month to keep your utilization ratio as low as possible.

Myth: You should keep your overall credit utilization ratio below 30%.

Fact: You should keep your overall utilization ratio as low as possible—and don’t forget about your individual utilization ratios.

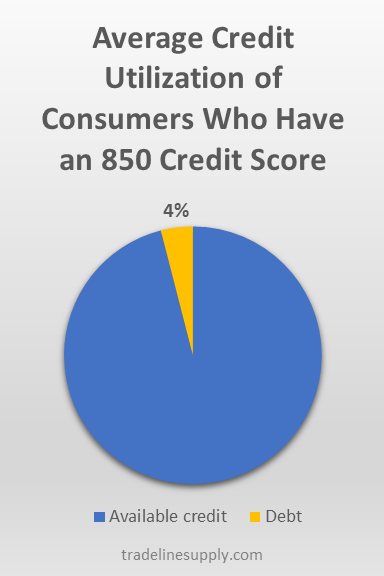

The average credit utilization rate of consumers who have an 850 FICO score is about 4%.

While the most often-repeated credit advice says to keep your credit utilization below 30%, unfortunately, that’s not the magic number.

In fact, there isn’t really a magic number at all when it comes to utilization ratios. The best rule of thumb is to keep it as low as possible.

Creditcards.com says that the ideal utilization is having all of your cards report a zero balance, with the exception of one card in the 1-3% range to show that you are actually using credit.

However, it’s still possible to have a perfect credit score while having an overall utilization ratio of about 4%, as we mentioned in “How to Get an 850 Credit Score.”

If you can’t keep your utilization between 0-10%, then try to shoot for around 20%, not 30%.

In addition, don’t forget to take into account the utilization of your individual revolving accounts. Having accounts with high individual utilization ratios can still bring down your credit score, even if your overall utilization ratio is in the ideal range.

You can read more credit utilization tips in our article, “What Is the Difference Between Individual and Overall Credit Utilization Ratios?”

Video: Why You Shouldn’t Believe This Myth About Credit Utilization

In the video below, credit expert John Ulzheimer addresses misconceptions about credit utilization and gives you the facts you need to know.

Want to see more videos about credit myths? Check out our Credit Myth Busters playlist on YouTube!

Myth: Shopping around for the best rates on a loan will hurt your credit score.

Fact: Getting loan estimates from multiple lenders will not hurt your score if you complete the process within a specific time window.

Credit scoring algorithms understand that it’s smart to shop around for the best rates on a loan, not risky. Therefore, credit scores typically have ways of preventing the series of multiple inquiries that result from this process from hurting your score excessively.

If you are applying for student loans, mortgages, or auto loans, FICO scores allow a certain time frame for you to shop around, only counting one hard inquiry to your credit report for this time period. For older FICO scores, the time window is 14 days; for newer FICO scores, the time window is 45 days.

In addition, FICO scores have a 30-day hard inquiry “buffer,” meaning that the algorithm ignores any inquiries that occurred within the past 30 days when calculating your score.

VantageScore uses a simpler method: it groups all inquiries made within a 14-day window of each other together and counts those all as one inquiry, regardless of what types of accounts the inquiries were for.

Myth: You can fix your credit by disputing everything on your credit report.

Fact: Disputing everything on your credit report could get you into legal trouble and may not even help your credit.

If there is information on your credit report that is inaccurate, outdated, incomplete, or unverifiable, of course, you would want to dispute those inaccurate items with the credit bureaus. But it’s not necessarily a good idea to dispute negative items on your credit report that are accurate and timely.

First of all, the derogatory items won’t necessarily get deleted from your credit report, especially if you don’t provide proof that they are inaccurate. They might just get updated with the correct information, or they may get deleted temporarily until an investigation determines the items are valid and they go right back on your credit report.

Furthermore, the credit bureaus don’t have to investigate disputes that are deemed “frivolous,” and they could decide that some of your disputes are frivolous if you are disputing every item in your credit file, regardless of accuracy.

Plus, lying on a credit dispute could be considered fraudulent. According to the FTC, “No one can legally remove accurate and timely negative information from a credit report.”

Even if you were to get away with disputing everything on your report, this might not necessarily help your credit as much as you hoped. If you’ve gone through an aggressive credit sweep and have nothing left on your report, then you essentially have no credit history and likely no credit score, which could be just as problematic as having bad credit.

Myth: CPN numbers can be used in place of social security numbers to create a new, clean credit file.

Fact: CPNs are illegal and using one to apply for credit is a federal crime.

Using a CPN to apply for credit is a federal crime. Photo via seniorliving.org.

Although you might have heard some people claim that “credit profile numbers” or credit privacy numbers” are a legitimate way to protect your privacy or wipe your credit slate clean, in reality, there is no legitimate or legal source for CPN numbers.

Most of the time, these numbers are either fake social security numbers that have not been created yet or real SSNs that have been stolen from children, the elderly, deceased people, people who are incarcerated, and people who are homeless. Either way, using a CPN means getting involved in identity fraud, which is a federal crime.

The Social Security Administration and the Federal Trade Commission have both explicitly stated that applying for credit using a CPN is illegal and that those who sell CPNs are scamming consumers.

Learn more about the dangers of CPNs in our article on the topic.

Myth: The credit score you check online is the same one lenders see when they pull your credit.

Fact: Lenders often do not use the same credit scores that are provided for free online.

When you check your credit score for free online, the credit score you see is most likely going to be a VantageScore. This is the score most commonly used by free online services such as Credit Karma.

The majority of lenders, however, primarily use FICO scores, although some lenders are now starting to use VantageScore. Just keep in mind that the score you see online may not be the same as the score lenders see, as there can often be a significant difference between your VantageScore and your FICO score.

If you want to check your FICO score for free, check with your credit card issuer, since many banks now offer this service free of charge.

Myth: If you don’t have any debt, you will have a good credit score.

Fact: You need to use credit to build your credit score.

Having good credit doesn’t just come down to the amount of debt you have—that’s just one part of your credit score. Payment history is the most important part of a credit score, so if you’ve never had debt and you don’t have any payment history, you might not even have a credit score at all.

To get a good credit score, you have to use some form of credit and demonstrate that you can use credit responsibly by building up a positive payment history over time.

Myth: There’s no need to check your credit report until it’s time to apply for a big loan.

Fact: It’s important to monitor your credit regularly.

Waiting to check your credit score until you need to apply for credit is a mistake because there could be errors on your credit report bringing your score down. Studies estimate that about one-fifth of consumers have at least one error on their credit report, some of which could be serious enough to result in higher interest rates, less favorable loan terms, or being denied credit.

It’s important to keep an eye on your credit so that you can correct errors and fight fraud as soon as possible instead of waiting until it’s too late. There are several reputable websites that offer free credit monitoring, such as Credit Karma, and some credit card issuers also provide free access to your credit report and credit score.

In our article on what you need to know about credit reports, we explain that most of the time, consumers are allowed to access their credit reports from each of the three major credit bureaus once a year for free by going to annualcreditreport.com.

However, during the COVID-19 pandemic, since it has caused so much financial stress and devastation for many Americans, the credit bureaus are currently allowing consumers to check their own credit reports for free up to once a week until April 20, 2021.

Myth: A late payment will make your score go down by 50 points.

Fact: There is no set amount of points that is associated with any particular item on your credit report.

While it is certainly possible that a 30-day late payment could cause a 50-point drop (or more) in someone’s credit score, this is not always going to be the case. There is no fixed number of points that your score will go up or down by for each item on your credit report. Rather, the way in which a late payment affects your score is always going to depend on your individual credit profile.

There is no set amount of points associated with missing a payment.

Credit scoring algorithms are very complex and they incorporate hundreds of variables, such as how recent the late payment is, whether you have other late payments in your credit history, and how severe the delinquency is, not to mention the myriad other variables associated with the other categories within a credit score.

Because delinquencies on your credit report are always going to be relative to whatever else is in your file, there is a “diminishing returns” effect where the first late payment hurts your score the most and each subsequent late payment tends to have a smaller impact.

Someone who has a high credit score and has never missed a payment before is going to experience a severe drop from their first missed payment, whereas someone who already has late payments on their record and a lower credit score is going to be hurt less by a subsequent late payment.

According to credit expert John Ulzheimer in a blog article, “Delinquencies, like inquiries, do not have independent value… It is entirely inappropriate and incorrect to say that ‘X’ lowered my score by ‘Y’ points.”

He continues, “The late payment didn’t lower your score but because adding a late payment to a credit report moves other things around it caused your score to be different than it was before the late payment was added. If your score is 50 points lower it’s not as if the new late payment lowered your score 50 points…but because the addition of that item caused a different evaluation of EVERYTHING on your credit reports…the new reality for you is 50 points lower.”

The same principle goes for other items on your credit report as well, not just late payments.

Myth: You don’t have to worry about your kid’s credit.

Fact: You should keep an eye on your kid’s credit report, too.

Make sure you monitor your kid’s credit in addition to your own.

The proliferation of scammers and hackers stealing people’s private information means even your kid’s credit profile could be at risk of identity theft. When people use “credit profile numbers” (CPNs), for example, these numbers are often real social security numbers stolen from children.

You don’t want to wait until your child is grown up and ready to apply for credit to realize they have bad credit as a result of identity theft. Consider freezing your kid’s credit to prevent fraudsters from opening accounts in their name.

In addition to monitoring and protecting your child’s credit, you can also help your child start to build credit early in life through strategies like credit piggybacking. See “At What Age Can You Start Building Credit?” for additional guidance on this topic.

Myth: Everyone’s credit score is calculated in the same way.

Fact: Credit scores have “scorecards” that categorize consumers and score them differently.

You already know that credit scoring algorithms are extremely complex, but what many people don’t know about is the “scorecards” or “buckets” within each credit scoring model. These “buckets” consist of different categories of consumers.

For example, according to John Ulzheimer, “There are scorecards for thin files or those with few accounts, bankruptcy, derogatories, and those with clean credit files… Comparing like populations gives this population an opportunity to be considered based on [the] behavior of that group rather than a comparison to another, better group.”

The credit scoring formula is different for each bucket. In other words, items on your credit report can be treated differently based on which scorecard you fall into.

Sometimes your credit score changes in a way that you don’t expect. For example, perhaps an inaccurate collection account got deleted off of your credit report and your score went down, instead of up. This could be because you changed scorecards as a result of the deletion, causing your credit score to be calculated in a different way. Essentially, you might now be at the bottom of a different bucket instead of at the top of your previous bucket.

It’s always good to keep the concept of scorecards in mind, especially when trying to predict any kind of change to your credit score. You can never guess exactly how your score will change because of all the complexities and trade secrets that go into credit scores.

John Ulzheimer reveals how these buckets work in one of our Credit Countdown videos on our YouTube channel!

Conclusions

Unfortunately, there are tons of credit myths out there, and believing them may lead you to mismanage your credit and eventually end up with poor credit. We hope that this article helped to dispel many of the misconceptions about credit and helped you get started on the path to better credit.

What credit myths have you heard of? Did you previously believe any of these? We’d love to hear from you, so share your experience with us in the comments!

{kind=link}

{kind=link}