Credit Building for Military Members

How to Build Credit for a Car Purchase

07/29/2022

The Cost of Being Queer

08/07/2022

As a member of the military, you face tough challenges on a regular basis. The tenacity and perseverance you build during your career can translate into other aspects of your life. One place to channel your energy is into building a great credit score.

As a member of the military, you face tough challenges on a regular basis. The tenacity and perseverance you build during your career can translate into other aspects of your life. One place to channel your energy is into building a great credit score.

The right credit score serves as a building block for a solid financial future. And it’s possible to take your credit score to new heights whether you are starting from scratch or rebuilding from a low point. If you are ready to turn your credit score into a tool for your financial situation, then keep reading to learn the steps military members can take to tackle credit building.

Why You Should Build Credit in the Military

Before we jump into how you can build credit in the military, let’s explore why you should even bother in the first place.

After all, building credit can take a bit of effort and some time to see real results. Here’s how putting in the effort required to build good credit will pay off.

Unlock Better Interest Rates

The most obvious benefit of building credit is the potential to unlock attractive financing opportunities. Not only can the right credit score help you unlock access to financing, but a good credit score can also help you get better interest rates for a variety of loan products.

When it comes to interest rates, a small difference can add up to big savings.

For example, let’s say that you have a fair credit score and wait to finance a car purchase for the average loan amount of $39,540. You take out a loan for 60 months with a 5% interest rate. Over the course of the loan, you’ll pay $5,230 in interest with your $746 monthly payments.

But what if you had an excellent credit score? You might be able to lock in a 3.5% interest rate for the same loan amount. With that, you’d only pay $719 each month and $3,618 in interest over the life of the loan. That leads to over $1,600 in savings over the life of the loan.

Access Premium Rewards Credit Cards

A premium credit card comes with plenty of perks to suit your lifestyle.

Depending on your preferences, you might choose a travel rewards credit card with built-in perks for travelers. Or you might want to open a credit card that offers significant cash back opportunities on your groceries and gas purchases.

But you’ll need a great credit score to access premium credit cards. Most credit card issuers require at least a good credit score to open a card with all of the perks you want.

Of course, you’ll need to use your credit card responsibly to get the most out of your rewards. Responsible credit card usage includes paying your bills on time and keeping the balance low.

Put Homeownership on the Table

Homeownership represents the pinnacle of the American dream for many families. If you are interested in homeownership, then building a good credit score is essential.

Although the U.S. Department of Veterans Affairs doesn’t set a specific credit score requirement, most lenders require a solid score to finalize a mortgage. In fact, the median credit score for home buyers taking out a mortgage in 2021 was 786, according to the Federal Reserve Bank of New York.

Even though it’s still possible to obtain a mortgage with a mediocre credit score, you may save thousands over the life of your loan by working on your credit score now. If you are considering homeownership in your future, then don’t miss the chance to build your credit score now. The choices you make now can lead to a better credit score when you are ready to buy a home.

What Makes a Good Credit Score

A good credit score can clearly make the financial aspect of your life much easier. But what makes a credit score a good one?

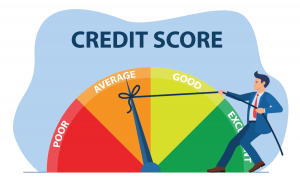

FICO credit scores are issued on a scale of 300 to 850. Here’s the breakdown of the FICO scores:

- Poor: Credit scores between 300 and 579 are considered poor.

- Fair: Credit scores between 580 and 669 are considered fair.

- Good: Credit scores between 670 and 739 are considered good.

- Very good: Credit scores between 740 and 799 are considered very good.

- Excellent: Credits cores between 800 and 850 are considered excellent.

It’s also possible to have no credit score at all. If you are credit invisible, it means you haven’t had a loan or used a credit card in years. Without enough information to issue a credit score, lenders are often wary of lending to credit invisible borrowers.

Curious about what factors go into a good credit score? The building blocks of a FICO score include:

- Payment history: Payment history represents 35% of your FICO score, making it the most important factor. Making on-time payments is a critical component of a good credit score.

- How much you owe: This includes how much revolving and installment debt you have.

- Length of credit history: The average age of your accounts represents 15% of your FICO score. The older your credit accounts, the better off your credit score will be.

- Credit mix: You’ll need to have a mix of revolving and installment credit accounts to show creditors you can responsibly manage both types of debt. The credit mix accounts for 10% of your FICO score.

- New credit: When you open new credit accounts or make credit inquiries, that can hurt your credit score. But this factor only accounts for 10% of your FICO score.

If you manage the factors above responsibly, you can unlock a great credit score.

How to Build Credit in the Military

The military offers plenty of interesting experiences. One thing to add to your list is building a credit score to be proud of. With the right credit score in your back pocket, you can unlock better financing opportunities which can really give your budget a break.

If you are ready to add a good credit score to your financial arsenal, implement the following strategies.

Get Credit for Your Alternative Payments

Even if you pay your bills on time, you might not get credit for those actions if it’s not a traditional credit account. But since a responsible record of on-time payments is so important to your credit score, it’s a good idea to get creative about your alternative bill payments.

It’s possible to get non-traditional credit accounts added to your credit report. A few potential payments that can be reported to the credit bureaus include your utilities, rent, cellphone service, or subscription streaming services.

You won’t get credit for any of these alternative payments unless you enlist the help of a service. For example, you can sign up for Experian Boost. The free service pores over your bank records to spot instances of on-time payments. When implementing Experian Boost, the average user saw their credit score increase by 13 points. If you’d like to build credit with rent, other options include Rental Kharma and LevelCredit.

But keep in mind that to get credit for paying any of these bills on time, the account must be in your name. For example, if you are splitting the cost of a popular streaming service like Netflix, you won’t get credit unless the account is in your name.

Pay Off Debt

Debt is a pervasive financial issue that will impact more than your credit score. A large amount of high-interest debt can shake your financial foundation to its core. With debt payments eating up a large part of your income, it can be challenging to keep up with on-time payments.

But paying off debt isn’t always easy. If you aren’t sure how to tackle your debt, explore the snowball and avalanche strategies.

The snowball method advises paying off debts starting with the smallest balance first. After you eliminate this small debt from your books, you can start working on the debt with the next highest balance. With each debt you eliminate, you can add its monthly payment to your debt snowball. It gets easier to tackle your debts as your snowball grows.

On the other hand, the avalanche method focuses on paying off your debt with the highest interest rate first. After you pay off this debt, you can move on to the debt with the next highest interest rate. The avalanche will grow as you tackle debts. Although this option is more efficient, you won’t immediately get the small wins that can motivate you to the finish line.

Either option gives you a framework to tackle your debts one at a time until debt is out of your life for good.

Make On-time Payments a Priority

As we mentioned, your payment history accounts for 35% of your FICO score. So, a record of on-time payments is a critical factor when building a good credit score.

Depending on your situation, it might be a challenge to make on-time payments. Consider setting up autopay to avoid accidentally missed payments. The helping hand of technology will prevent any mistakes.

But sometimes, a crunched cash flow is the culprit of a missed payment. Typically, you’ll know in advance if you aren’t going to be able to make a payment due to a lack of cash.

If you see that problem on the horizon, reach out to your lender as soon as possible. As a customer with a regular history of on-time payments, they might be willing to work with you by offering an extension or temporary forbearance. It never hurts to ask!

Consider a Secured Credit Card

A secured credit card can help you build credit. It’s typically easy to open a secured credit card because you’ll be responsible for making a deposit that essentially acts as your credit limit. The lender has access to this cash as collateral if you miss a payment.

When making on-time payments, a secured credit card offers the chance of building credit. However, you’ll need to keep a careful eye on your credit utilization ratio. The usually low limits make it easy to rack up a high credit utilization ratio.

Consider a Credit-builder Loan

A credit-builder loan tackles two financial goals with one product. You can build credit and savings at the same time.

But a credit-builder loan isn’t your typical loan product. When you take out a credit-builder loan, you won’t receive any funds upfront. Instead, the lender opens a savings account or certificate of deposit earmarked for your savings.

Each month, you’ll make payments to the lender. From there, they’ll put the principal portion of the loan into your designated account. When you make payments, the lender reports this activity to the credit bureaus. And when the loan term is up, you’ll get access to the savings you’ve built.

It’s possible for a credit-builder loan to hurt your credit score. If you don’t make on-time payments, this loan product will have a negative impact on your score.

Lower Your Credit Utilization Ratio

A high credit utilization ratio will drag down your credit score. Keeping your credit utilization under 10% is ideal. Any higher than that and this factor could start to bring down your credit score, but if that’s not a realistic goal for you, just keep it as low as you can.

If you have a high debt burden on your revolving accounts, take action to pay off this debt.

Try Credit Repair

Credit repair offers an opportunity to remove any inaccurate information from your credit report. Most mistakes on your credit report will have a negative impact on your score. After all, it’s unlikely that someone who has stolen your identity will make on-time payments.

If you spot mistakes on your credit report, you can work with a reputable credit repair service to have them removed. Or you can tackle this project yourself. Essentially, you’ll just need to reach out to the credit bureaus and provide information about the mistake.

The credit bureau will have 30 days to respond. They’ll either fix the issue or send you a letter about why they think it’s valid information. Credit repair can help you erase things that are dragging your credit score down.

The Bottom Line

A good credit score can open the door to exciting financial opportunities. But building a solid credit score takes time. So, it’s important to start building as early as possible. If you have a reason to use credit on the horizon, take action to build your credit score as soon as possible.

What do you think of this article about building credit in the military? Let us know with a comment below!

{kind=link}

{kind=link}