How to Build Credit Without a Credit Card

How to Increase Your Credit Limit

05/04/2023

What to Do if You Experience Credit Card Fraud

05/12/2023

A good credit score is a key to accessing financing options on major purchases. Building credit can be easier said than done. One popular way of building credit is to use a credit card. But that’s not the only option.

A good credit score is a key to accessing financing options on major purchases. Building credit can be easier said than done. One popular way of building credit is to use a credit card. But that’s not the only option.

If you aren’t interested in the spending temptations that a credit card brings, then it’s possible to avoid one altogether. Here’s a closer look at how to build credit without a credit card.

Can You Build Credit Without a Credit Card?

When you are building credit, one of the most popular strategies is to responsibly manage your credit card. But it’s entirely possible to build credit without a credit card at all.

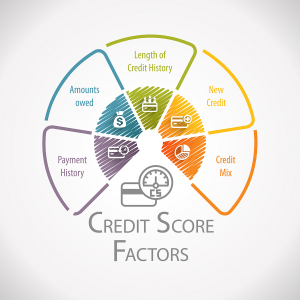

Your credit score is based on the responsible credit management of all of your credit accounts. The score is a 3-digit number that represents your credit risk. Here are the five factors that impact your credit score:

- Payment history: Payment history represents 35% of your FICO score. With that, it’s the most important piece of your credit score. Making on-time payments for all of your credit accounts leads to a positive impact on your score.

- Utilization ratio: Your credit utilization ratio is a measure of the amount of outstanding debt you have compared to your revolving account balances, expressed as a percentage. So, a lower utilization ratio means a better credit score.

- Length of credit history: The length of your credit history represents 15% of your credit score. A longer credit history often leads to a higher credit score.

- Credit mix: Not all credit accounts are managed in the same ways. Creditors want to ensure the borrower can manage different credit account types well. A mix of credit including both installment loans and revolving credit accounts will boost this factor which represents 10% of your score.

New credit inquiries: Last but not least, recent credit inquiries will account for about 10% of your FICO score. If you’ve made any credit inquiries within the last 6 to 12 months, that’s a risk factor that could lower your score.

New credit inquiries: Last but not least, recent credit inquiries will account for about 10% of your FICO score. If you’ve made any credit inquiries within the last 6 to 12 months, that’s a risk factor that could lower your score.

New credit inquiries:

New credit inquiries: After taking a look at the factors that compose your credit score, it’s clear that you don’t necessarily need a credit card to build your credit score. Instead, you’ll need to make a concerted effort to responsibly manage other credit accounts you obtain.

Reasons to Build Credit Without a Credit Card

We’ve established that it’s possible to build credit without a credit card. But why shy away from opening a credit card?

There’s nothing wrong with getting a credit card to build credit. But here are some good reasons to steer clear of credit cards.

Avoid the Temptation of Spending to Your Limit

When you open a credit card, the issuer will determine a spending limit based on your income and other factors. In some cases, the spending limit is relatively high when compared to your regular monthly spending.

A high credit limit might sound like a great thing. But it can make it extremely tempting to overspend. After all, it’s very easy to swipe your credit card for a splurge.

Although you’ll have to make minimum monthly payments, you won’t be required to pay off your entire balance each month. With that, it’s very easy to slide down the slippery slope of credit card debt. So, it’s not surprising that the average credit card debt for a U.S. family is $6,194.

If you are worried about overspending due to a high credit card limit, then it’s a good idea to find another credit-building opportunity.

Avoid High Interest Rates

Credit cards have notoriously high interest rates. As of 2022, the average credit card interest rate is 16.17%. That’s an incredibly high rate!

If you slip into credit card debt, it can be difficult to get out with such a high interest rate attached. Even just carrying a small balance on your credit card can be an expensive choice.

Avoid Expensive Fees

In addition to the high interest rates, most credit cards come with expensive fees. A few common fees attached to credit cards include:

- Annual fee

- Late payment fee

- Foreign transaction fee

- Balance transfer fee

- Cash advance fee

- Over-the-limit fee

- Returned payment fee

Late payment fee

Late payment feeAs a credit card user, you’ll likely run into one of these budget-ruining fees at some point.

Accounts That Build Credit Without a Credit Card

If you aren’t interested in getting a credit card, there are other account types that can help you build credit. The list below offers a look at some of the other accounts you can use to build credit.

Car Loans

When you take out an auto loan, you’ll be required to make monthly payments. If you make on-time payments, that will lead to an increased credit score.

Cash buyers won’t be able to take advantage of this credit-building opportunity.

Student Loans

Student loans are an unavoidable part of life for many college students. After graduation, the required monthly payments kick in after a short grace period. In many cases, student loan payments are a crunch on fresh college grads. But consistent on-time payments can help you improve your credit score.

Rent Payments

In most cases, your landlord won’t report your monthly rent payment to a credit bureau. However, there are some unique services you can sign up for that will report your rent payments for you.

For example, you could work with Level Credit to get your rent payments reported. Although there is a cost involved, the boost to your credit score could be worth it.

Utility Payments

Utility payments are another monthly bill that you are likely paying on time. If you have utility accounts in your name, you can have these payments added to your credit report.

If you are interested in this option, then consider signing up for Experian Boost. It’s a free service that may be able to increase your credit score by reporting your on-time payment history with non-traditional accounts.

Subscription Payments

Subscription payments to streaming services are another non-traditional way to improve your credit score. A few popular subscriptions to get credit for include Netflix, Disney+, and HBO.

If you have subscriptions in your name, then Experian Boost can help you get credit for these on-time payments. According to Experian Boost, the service has helped the average user raise their credit score by 13 points.

Credit-builder Loans

A credit-builder loan is a product specifically designed to help you build credit. It’s a very useful tool for those with no credit or very low credit scores.

Unlike a traditional loan product, you won’t receive a lump sum principal payment upfront. Instead, you’ll start making payments right away. With each payment, the lender will save the principal portion of the payment in a specialized savings account or CD. The interest portion of the payment will go to the lender.

Throughout the loan term, the lender will report your payments to the credit bureaus. At the end of the loan term, you’ll receive the lump sum loan amount. In some ways, you can think of this as a forced savings opportunity that helps you build credit at the same time.

Here’s where you can learn more about credit builder loans.

Become an Authorized User

When you become an authorized user on a well-managed credit account, that can be a boon to your own credit. If you have a family member or friend that is willing to add you as an authorized user to their credit accounts, this can help you build credit without having to open a credit card of your own.

Installment Loans

Installment loans of all kinds can help you build credit. A few examples of installment loans include car loans, mortgages, and personal loans. When you make on-time payments to any of these installment loans, that can be a positive influence on your credit score.

Buy Now Pay Later Services

Buy Now Pay Later (BNPL) services allow you to space out the cost of a purchase through a major retailer.

So, instead of paying for a $100 item all at once, you can break up that purchase into several payments. Depending on the amount of your purchase and the BNPL service, the repayment timeline will vary.

In some cases, the BNPL service will report your payments to the credit bureaus. A few that report at least some of their loans to credit bureaus include Affirm, Sezzle, and Klarna. If you are making on-time payments to the service, that could lead to a boost in your credit score. However, most BNPL loans are not reported to the credit bureaus at this time, although the credit bureaus are working on eventually incorporating BNPL data into consumers’ credit files.

Want to learn more about Buy Now Pay Later services? Take a look at our full guide.

How to Build Credit Without a Credit Card

You can build a better credit score through a wide range of credit accounts. If you are looking to avoid having a credit card in your wallet, a better credit score is still a possibility. That’s especially true if you follow the game plan below.

Here’s how to build credit without a credit card.

Get Credit for Alternative Payments

Although you may not have a traditional credit account, it’s likely that you have some bills to pay each month. If you pay for rent, utilities, subscription streaming services, or a cellphone plan, those alternative payments could be the key to painting a picture of a reliable borrower.

In general, you won’t automatically get credit for these payments. But if you know that these bills are being paid on time each month, then it’s worthwhile to find a service that will report these payments to the credit bureaus.

One option is Experian Boost. The free service will comb through your payment history to determine your payment history. But you’ll need to have these non-traditional credit accounts in your own name. So, if you are paying a roommate for half of the utility bill, you won’t be able to get credit for that payment.

Read more about alternative credit data in our article.

Make On-time Payments

A history of on-time payments is the biggest factor in your FICO score. Of course, other factors will influence your credit score. But a pristine record of on-time payments will go a long way.

If possible, make on-time payments for all of your credit accounts. One way to do this is by setting up an automatic payment. When auto payments are on, you won’t accidentally forget to pay the bill.

But if you are struggling to come up with the funds for a payment, then consider reaching out to your lender. In some cases, they may be willing to work with you to avoid a missed payment. For example, they could change the due date or grant a temporary forbearance to prevent a missed payment. Reach out to your lender as soon as you know that you might miss a payment. You might be surprised to find that many lenders are willing to help out, especially if you’ve been a reliable customer in the past.

Credit Repair

Credit repair is the process of removing incorrect information from your credit report. In most cases, mistakes on your credit report will drag your score down.

For example, if someone steals your identity to open a credit card, they won’t be making on-time payments. So, when that information is removed, it can stop hurting your credit score.

You can work with a reputable credit repair service to remove incorrect information from your credit report. But it’s also possible to tackle this on your own.

If you decide to go it alone, start by identifying any mistakes in your credit report. When you spot mistakes, contact the appropriate credit bureaus to ask for a correction. Be prepared to provide details about the mistake. In most cases, removing one or two mistakes is very manageable. But if you’ve been the victim of extensive identity theft, then you may want to hire a credit repair service.

Here’s where you can learn more about DIY credit repair.

The Bottom Line

If you want to build credit without opening a credit card, that’s definitely an option. Although a credit card is a useful credit-building tool, it’s not the only choice for credit-builders. As you work to build credit, consider using a combination of multiple options for the best results.

{kind=link}

{kind=link}