How to Avoid Emotional Spending

What to Do if You Experience Credit Card Fraud

05/12/2023

How to Get an 850 Credit Score [Infographic]

05/31/2023

Emotional spending is one personal finance issue that many struggle with. According to a NerdWallet survey, 49% of Americans said emotions have caused them to spend more than they can reasonably afford. With almost half of Americans struggling with emotional overspending, you aren’t alone if you are facing this issue.

While emotional spending is common, that doesn’t mean it’s good for your financial picture. In fact, too much emotional spending can lead to negative financial consequences.

Let’s explore the impacts of emotional spending. Plus, we’ll give you steps you can take to avoid emotional spending.

What Is Emotional Spending?

Before we talk about how to stop emotional spending, it’s critical to define this common issue. Essentially, emotional spending boils down to buying something that you likely don’t need to spark a particular feeling. For example, you might spend to spark some happiness after a stressful day. Or you might spend to celebrate a small accomplishment.

Emotional spending looks different for everyone. But spending as part of an emotional reaction to something is the thread that ties all emotional spending together. Typically, emotional spending takes the form of an impulse buy that doesn’t have a place in your budget.

Potential Impacts of Emotional Spending

On the surface, emotional spending might seem harmless. After all, purchasing a pick-me-up to feel better after a long day of work might not seem like a big deal. But the reality is that emotional spending can have a big impact on your financial situation.

Here’s a look at some of the potential financial impacts of emotional spending.

Too Much Spending

When emotions get involved in your spending decisions, it’s easy to spend more than you should. Instead of looking at your numbers-based budget, emotional spending relies on your feelings when determining whether or not to make a purchase. Although you might feel like you “need” or “deserve” something in the moment, overspending on emotional purchases can wreak havoc on your budget.

Most of us have been in an emotional spending situation that pushed us to spend too much. You might feel the pressure to overspend in pursuit of a feeling. If emotional spending becomes a regular habit, you’ll likely face bigger bills.

Credit Card Debt

If emotional spending pushes you to spend beyond your means, a credit card is an easy way to cover the purchases. When you reach for your credit card, swiping it through the terminal or typing in the details is easy enough.

But when your credit card statement arrives, you might not be able to pay off the entire balance in full. And that’s where the slippery slope of credit card debt starts. Sky-high interest rates combined with emotional spending make it very easy to fall into credit card debt. Unfortunately, it is often difficult to climb back out of credit card debt.

Negative Impact on Credit Score

When managing your credit, maintaining a low credit utilization ratio is important. Your credit utilization ratio is one of many factors that your credit score takes into account. If you are overspending with a credit card, you might not be able to pay off your balance in full each month. Instead, your credit card balance will be growing. As your balance grows, your credit utilization ratio balloons with it. Plus, the increasing payment might make it difficult for you to keep up with on-time monthly payments. This combination of factors might push your credit score down.

Negative Relationship With Money

Emotional spending ties your feelings to money. In many cases, emotional spending can lead to a bad relationship with money. If your emotional spending persists, it’s relatively common to develop uncomfortable feelings about money.

A bad relationship with money can cause you to avoid savvy money management strategies. In many cases, developing a better relationship with your money management can lead to smarter money decisions and good long-term money outcomes.

How to Avoid Emotional Spending

It’s clear that emotional spending often has a negative impact on our finances. If you want to cut out emotional spending from your life, that’s a great idea. Below are some strategies to help you avoid overspending.

Identify Your Spending Triggers

Emotional spending is spurred by different things for different people. You might have specific triggers that push you into overspending. For example, a stressful day at work might push you to stop for a shopping treat on your way home.

Here’s a look at some of the most common spending triggers:

- Fear: If you are nervous about something, you might resort to spending to combat this emotion. For example, someone who is worried about a work project might go overboard with the supplies.

- Achievement: If you hit a goal of any kind, you might be tempted to celebrate with a victory purchase. However, your budget might not be ready to absorb every small victory purchase along the way.

- Sadness: A case of the blues might push you to spark joy with an emotional purchase. In a way, it’s a smart move because our brains release endorphins when we make a purchase. But many of our budgets cannot handle sustained sadness spending.

- Jealousy: If you feel the pressure to keep up with the Joneses, that pressure might impact your spending choices. Someone spending more than they should to buy the newest and best things that outshine others might be facing jealousy spending.

- Guilt: If you feel like you let yourself or someone else down, you might channel that energy into buying comforting treats.

Everyone has unique spending triggers. Take some time to watch your spending behaviors. You might spot a common trigger that pushes you to overspend.

Redirect Your Spending Energy

When you know what your spending triggers are, you can redirect your spending energy into another form of healing.

After a bad day, it’s tempting to whip out your credit card. But redirecting your energy might look like going for a walk, journaling about your emotions, calling a friend, or cooking a healthy meal. Any of these alternatives won’t push you into credit card debt. However, you still might get the same level of emotional satisfaction out of the arrangement.

Get creative when finding new ways to redirect your spending energy into a positive choice.

Put Barriers Between You and Emotional Spending

Creating simple barriers can help you get a handle on your emotional spending. The right barriers will look different for everyone. But here are some ideas to get you started.

- Use the 24-hour rule: If you spot something that you absolutely want to have, hold off on the purchase for 24 hours. In many cases, you’ll forget about the item. But if you still have a reason to get the item, then you can consider moving forward with the purchase.

- Set a price limit: If you want the freedom to shop with emotions leading the way, put a cap on the costs. For example, you might decide to only spend $10 per week on impulse purchases.

- Take your credit cards out of your wallet: Instead of carrying around your credit cards, put them away in a safe place at home. If you want to make a purchase, you’ll have to think about it before even leaving the house.

Remove the Temptation to Overspend

If you are easily tempted to overspend, consider removing the temptation.

- Freeze your credit cards: If credit cards offer too big of a spending temptation, then freeze them. Don’t give yourself access to a tool that allows you to spend too much.

- Set up automatic transfers: If a pile of cash in your checking account represents an invitation to overspend, move the money from your checking to your savings account. You can put this on autopilot so that each paycheck is automatically distributed into the appropriate accounts.

- Unsubscribe from email lists: Getting an email from your favorite store every day might trigger emotional overspending. Remove the temptation by unsubscribing from the email list.

- Set up a budget: A budget can help you avoid overspending. When you have a clear idea of what you have available to spend each month, you might be swayed from some emotional spending decisions.

Create a “Treat Yourself” Fund

For many of us, emotional spending is deeply engrained in our spending patterns. Instead of stamping out the habit entirely, creating a “treat yourself” fund is a helpful compromise. Essentially, the money within your “treat yourself” fund is designated for emotional spending. If you have a bad day or want to celebrate an achievement, the fund is there to cover the costs.

An appropriately sized “treat yourself” fund is actually a helpful financial tool. It allows you to account for other financial goals before putting money into this fund. For example, this fund might help you save for other goals while still having the option to treat yourself without guilt when you need the pick-me-up.

Be Patient With Yourself

As you work to restrain your emotional spending, it’s important to realize this process takes time. Although you might create a great system to reign in your emotional spending, it’s natural to slip up along the way. When you run into a mistake, be patient with yourself. Take a minute to learn the lesson, then try to move on from any negative thoughts.

Frequently Asked Questions

Can Spending Money Be a Coping Mechanism?

Yes. It’s possible to develop an overspending habit as a way of coping with uncomfortable feelings—but this coping mechanism will not solve larger emotional problems in the long run.

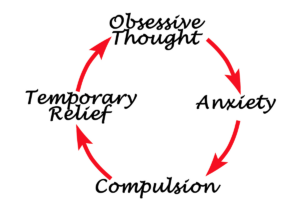

How Do You Deal With Obsessive Spending?

If you are struggling with overspending, try to get help from your support network. Additionally, remove temptations by getting rid of your credit cards and avoiding online shopping.

The Bottom Line

Emotional spending can wreak havoc on your financial plans. The first step to making a change is recognizing an issue. If you are ready to avoid emotional overspending, be patient with yourself as you move forward. With time, mindful spending practices should help you tame any emotional spending problems.

{kind=link}

{kind=link}

{kind=link}